By Michael Blank | Last updated: April 3, 2026

How value-add multifamily deals create cash flow, appreciation, and investor profits.

Watch the video: How Do Real Estate Syndications Actually Make Money

Have you ever looked at a real estate syndication and thought, Okay, but where does the money actually come from?

That is a fair question. A lot of investors see projected returns, preferred returns, IRRs, and equity multiples, but they do not always see the engine underneath it all. If you are a passive investor, you should understand that engine at a high level before you put capital into any deal.

I’m Michael Blank. I’ve spent years buying, investing in, and teaching multifamily real estate investing. In this article, I’ll walk you through how real estate syndications actually make money, why Net Operating Income (NOI) and cap rates matter so much, and how cash flow and appreciation work together in a value-add deal.

What Is the Main Way a Real Estate Syndication Creates Value?

The main way a real estate syndication creates value is by increasing a property’s NOI, or Net Operating Income. In commercial real estate, value is driven by income, not just by comparable sales.

Multifamily is valued more like a business than like a house. If the property produces more income, it is usually worth more. That is the core idea behind most value-add multifamily investing.

In many syndications, we buy an apartment building that has some clear room for improvement. Maybe the units are dated. Maybe the exterior needs work. Maybe the property is missing amenities that tenants want, like upgraded landscaping, a fitness room, or a dog park.

When we improve the property and operations, we can often justify higher rents and better collections. That pushes NOI higher.

Here is the simple relationship:

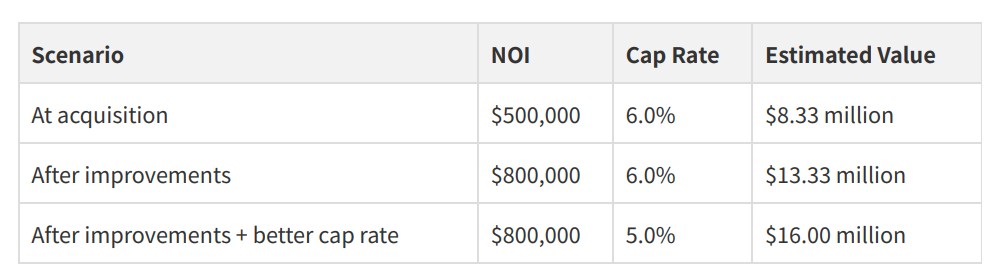

Property Value = NOI ÷ Cap Rate

So if a property has an annual NOI of $500,000 and the market cap rate is 6%, the value is about $8.33 million. If NOI grows to $800,000 and the cap rate stays the same, the value rises to about $13.33 million.

Why Do Cap Rates Matter So Much in Syndications?

Cap rates matter because even a small change in cap rate can create a very large change in value.

A cap rate, short for capitalization rate, is the return a buyer expects based on a property’s income. There is an inverse relationship between cap rates and value: when the cap rate goes down, the value goes up, assuming NOI stays the same.

You can think of it this way. A rougher property in a weaker area usually has more risk, more management friction, and more uncertainty. Because of that, buyers often want a higher return. That means a higher cap rate and a lower value.

A cleaner, stronger, more stable property in a better location may command a lower cap rate because buyers are willing to accept a lower return for lower perceived risk.

Now go back to the earlier example. If NOI rises to $800,000 and the cap rate compresses from 6% to 5%, the value jumps from about $13.33 million to $16 million. That is a massive change created by improvements in both income and market perception.

How Do Investors Actually Get Paid in a Syndication?

Investors typically get paid in two ways: cash flow during the hold period and profits when the property is refinanced or sold.

The first piece is cash flow. Once the property produces income above operating expenses and debt service, the remaining distributable cash can be paid to investors based on the deal structure.

The second piece is appreciation. If the sponsor executes the business plan well, the property becomes more valuable over time because NOI has grown. When the property is sold, investors receive their share of the proceeds after debt payoff and other closing adjustments.

In some deals, investors may also benefit from a refinance if the property’s value has increased enough to return part of the original capital while still holding the asset.

The Three Main Sources of Investor Returns

-

Cash Flow: Ongoing distributions during the hold period, funded by property operations after expenses and debt service.

-

Forced Appreciation: Value created by raising NOI through renovations, rent growth, and better management.

-

Sale or Refinance Proceeds: Investor profits realized when the property is sold or recapitalized after the business plan is executed.

This also creates flexibility. If the market is weak at the planned exit date, a good property with healthy cash flow may be held longer instead of being sold at the wrong time.

What Should You Watch for as a Passive Investor?

As a passive investor, you should focus less on headline returns and more on the assumptions that drive them.

A deal can look great in a webinar. That does not make it durable. I would rather see a modest return projection with credible assumptions than a sky-high projection built on cap rate compression, aggressive rent growth, and perfect execution.

Here are a few questions I think you should ask before investing:

-

How exactly will this property’s NOI increase?

-

What renovations or operational changes support that plan?

-

Are the rent premiums proven in the submarket, or are they just hoped for?

-

What exit cap rate is being used, and why?

-

How much of the projected return comes from cash flow versus sale proceeds?

-

What happens if the market softens and the property needs to be held longer?

When you ask those questions, you move from being a spectator to being an informed investor. That is where you want to be.

Frequently Asked Questions

Q: Is a syndication’s profit mostly from rent increases?A: Often, yes, but not only from rent increases. The bigger driver is usually NOI growth, which can come from higher rents, lower expenses, better collections, better management, or some combination of all four.

Q: What is NOI in simple terms?

A: NOI stands for Net Operating Income. It is the property’s income after operating expenses, but before debt service and taxes. In commercial real estate, NOI is one of the key drivers of value.

Q: Why does a lower cap rate increase value?

A: Because value is calculated by dividing NOI by the cap rate. If NOI stays the same and the cap rate goes lower, the resulting value goes higher.

Q: Can a syndication still work if the property is not sold on schedule?

A: Yes. If the property has solid cash flow, the sponsor may be able to hold it longer and wait for a better sale environment. That is one reason strong operations matter so much.

Q: What is the biggest risk for passive investors to watch?

A: Unrealistic assumptions. A deal can break if the sponsor overestimates rent growth, underestimates expenses, or assumes an overly favorable exit cap rate without a strong basis.

Real estate syndications make money in a fairly simple way. We buy an underperforming property, improve it, raise the NOI, and create value. Along the way, investors may receive cash flow. At refinance or sale, they may also receive their share of the appreciation created by that business plan.

That is why I like value-add multifamily so much. It is not a story built on hype. It is a business plan built on operations, math, and disciplined execution. If you understand those three pieces, you can evaluate syndications with a much sharper eye and invest more confidently.

Author: Michael Blank is the CEO of Nighthawk Equity and a longtime apartment investing educator. He has helped thousands of investors understand and invest in multifamily real estate. Last updated: April 3, 2026.